First Class Fair Value Adjustment Consolidation Statement Of Financial Position And Balance Sheet

Consolidated Financial Statement At More Than Book Value

This article illustrates how consolidation adjustment journal entries in a comprehensive case setting should be prepared using an. As goodwill is not recognised separately from the investment under the equity method IAS 36 requirements for mandatory annual impairment test do not apply IAS 2842. Investment entities are prohibited from consolidating particular subsidiaries see further information below. However during the consolidation process a revaluation surplus is not created. Fair value adjustments at date of acquisition will affect the goodwill calculation. A business combination takes the form of either a statutory merger or a statutory consolidation. Any further adjustment to fair value subsequent to acquisition will affect post acquisition retained earnings reserves. This will ensure that the fair value of net assets is carried through to the goodwill and non-controlling interest calculations. Applying the Consolidation Exception Amendments to IFRS 10 IFRS 12 and IAS 28 amendments effective 1 January 2016. It shows the individual book values of both companies the necessary adjustments and eliminations and the final consolidated values.

This will ensure that the fair value of net assets is carried through to the goodwill and non-controlling interest calculations.

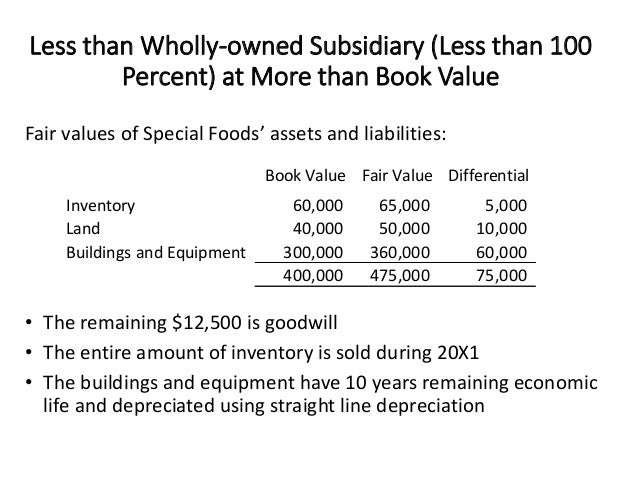

Any impairment of goodwill will be expensed through Consolidated Statement of Income. Applying the Consolidation Exception Amendments to IFRS 10 IFRS 12 and IAS 28 amendments effective 1 January 2016. Book Value Fair Value Buildings 10-year life 10000 8000 Equipment 4-year life 14000 18000 Land 5000 12000 Any excess consideration transferred over fair value is attributable to an unamortized patent with a useful life of 5 years. Consolidation worksheet is a tool used to prepare consolidated financial statements of a parent and its subsidiaries. So in other words were going to say that we have the parents books we have the subsidiaries books the parents books is reflecting and obviously we will do practice problems. Adjustments to prepare the consolidated financial statements.

Doing at consolidation adds considerable complication for future years - for example for fixed assets you then have to adjust depreciation and deferred tax each year as well as dealing with disposals. How a student actually makes the common consolidation adjustments should be similar regardless of what approach is used eg. Basically the subsidiaries books will basically be converted from a book value to a fair value at the point of purchase during the consolidation process. There is a consolidation adjustment in respect of the fair value adjustment on the PPE. Applying the Consolidation Exception Amendments to IFRS 10 IFRS 12 and IAS 28 amendments effective 1 January 2016. As goodwill is not recognised separately from the investment under the equity method IAS 36 requirements for mandatory annual impairment test do not apply IAS 2842. A business combination takes the form of either a statutory merger or a statutory consolidation. In terms of depreciable non-current assets a fair value adjustment is applied at the date of acquisition similar to applying the revaluation model under IAS 16 Property Plant and Equipment. It shows the individual book values of both companies the necessary adjustments and eliminations and the final consolidated values. The parent company buys an interest in a.

However during the consolidation process a revaluation surplus is not created. Adjustments to prepare the consolidated financial statements. Fair value is also used in a consolidation when a subsidiary companys financial statements are combined or consolidated with those of a parent company. A business combination takes the form of either a statutory merger or a statutory consolidation. Consolidation worksheet is a tool used to prepare consolidated financial statements of a parent and its subsidiaries. Doing at consolidation adds considerable complication for future years - for example for fixed assets you then have to adjust depreciation and deferred tax each year as well as dealing with disposals. There is a consolidation adjustment in respect of the fair value adjustment on the PPE. How a student actually makes the common consolidation adjustments should be similar regardless of what approach is used eg. In consolidation at December 31 2019 what net adjustment is necessary for Hogans Patent account. The carrying value or book value is an asset value based on the companys balance sheet which takes the cost of the asset and subtracts its depreciation over timeThe fair value.

Doing at consolidation adds considerable complication for future years - for example for fixed assets you then have to adjust depreciation and deferred tax each year as well as dealing with disposals. This article illustrates how consolidation adjustment journal entries in a comprehensive case setting should be prepared using an. So in other words were going to say that we have the parents books we have the subsidiaries books the parents books is reflecting and obviously we will do practice problems. How to include fair values in consolidation workings 1 Adjust both columns of W2 to bring the net assets to fair value at acquisition and reporting date. This video explains the how Non-Controlling Interest is valued using the Fair Value Method. Fair value is also used in a consolidation when a subsidiary companys financial statements are combined or consolidated with those of a parent company. Any further adjustment to fair value subsequent to acquisition will affect post acquisition retained earnings reserves. O Compare assets carrying amount to its recoverable amount Fair value cost to sell OR Value in use o Goodwill emerges during consolidation elimination entry so impairment loss is done on consolidation adjustment entry Journal entry o Dr Impairment loss o Cr Goodwill Journal entry impairment losses that are in prior periods. Because at the reporting date Singapore Co is owed 5000 by Marina Bay Co this is an intra-group item and this receivable is eliminated from the group accounts as a consolidation adjustment. Consolidation worksheet is a tool used to prepare consolidated financial statements of a parent and its subsidiaries.

It is a continuation of the Principles of Consolidation which use. Investment entities are prohibited from consolidating particular subsidiaries see further information below. There is a consolidation adjustment in respect of the fair value adjustment on the PPE. It shows the individual book values of both companies the necessary adjustments and eliminations and the final consolidated values. Fair value measurement clause added by Investment Entities. Any impairment of goodwill will be expensed through Consolidated Statement of Income. Fair value adjustments should be recorded at subsidiary level. Because at the reporting date Singapore Co is owed 5000 by Marina Bay Co this is an intra-group item and this receivable is eliminated from the group accounts as a consolidation adjustment. Book Value Fair Value Buildings 10-year life 10000 8000 Equipment 4-year life 14000 18000 Land 5000 12000 Any excess consideration transferred over fair value is attributable to an unamortized patent with a useful life of 5 years. Basically the subsidiaries books will basically be converted from a book value to a fair value at the point of purchase during the consolidation process.

Investment entities are prohibited from consolidating particular subsidiaries see further information below. The parent company buys an interest in a. However during the consolidation process a revaluation surplus is not created. Basically the subsidiaries books will basically be converted from a book value to a fair value at the point of purchase during the consolidation process. In consolidation at December 31 2019 what net adjustment is necessary for Hogans Patent account. Fair value is also used in a consolidation when a subsidiary companys financial statements are combined or consolidated with those of a parent company. Because at the reporting date Singapore Co is owed 5000 by Marina Bay Co this is an intra-group item and this receivable is eliminated from the group accounts as a consolidation adjustment. This video explains the how Non-Controlling Interest is valued using the Fair Value Method. It shows the individual book values of both companies the necessary adjustments and eliminations and the final consolidated values. There is only one way to adjust for a fair value adjustment it can however be presented differently depending on which approach is used.