Neat Income Tax Paid In Advance Cash Flow Three Sections Of The Statement Flows

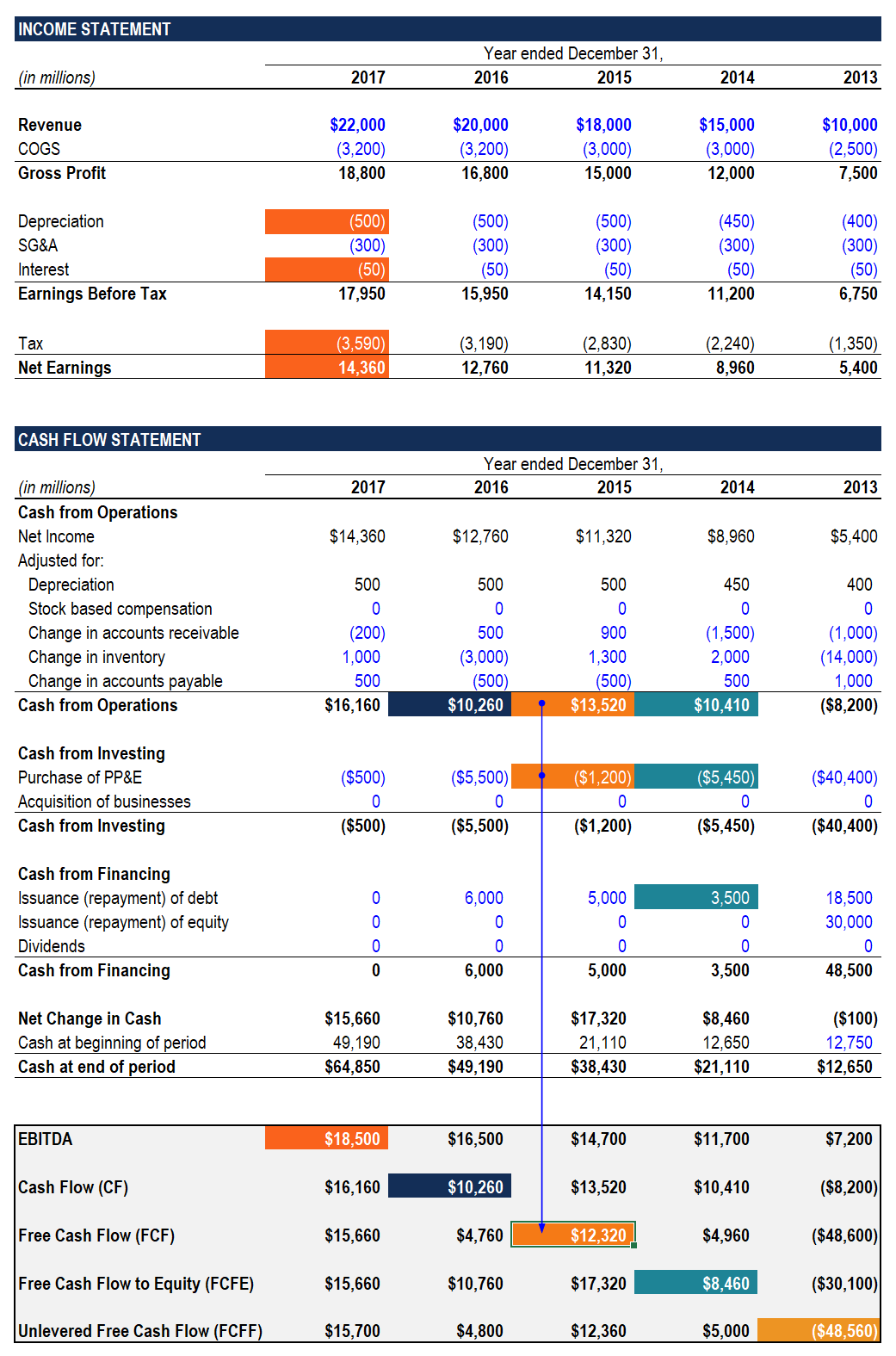

The Ultimate Cash Flow Guide Understand Ebitda Cf Fcf Fcff

If you are preparing cash flow as per direct method then you need to show actual payment ie. Income tax paid in advance cash flow. In either case they represent Inventory specifically held for. Interest paid in advance may arise as a company makes a payment ahead of the due date. Provision CY provision made - Cl. Income tax paid to be deducted after working capital changes is Rs1050311. However as the ending balance is only CU 16000 we can conclude that the amount of income tax paid must have been CU 25000. Net cash used in investing activities 470000 Cash flows from financing activities. If no payments were made the ending balance would be CU 41000. Others treat interest received as investing cash flow and interest paid as a financing cash flow.

Treatment Of Advance Income Tax In Cash Flow Statement.

IAS 12 implements a so-called comprehensive balance sheet method of accounting for income taxes which recognises both the current tax consequences of transactions and events and the future tax consequences of the future recovery or settlement of the carrying amount of an entitys assets and liabilities. Income tax paid in advance cash flow. The beginning balance of Current Tax Payable of CU 14000 is increased by the current portion of income tax expense CU 27000. The amount of taxes your company paid for the accounting period goes on the cash flow statement. Income tax paid to be deducted after working capital changes is Rs1050311. Cash flows from investing activities.

The method used is the choice of the finance director. Under IFRS there are two allowable ways of presenting interest expense in the cash flow statement. If no payments were made the ending balance would be CU 41000. Provision for Tax in Cash Flow Statement 1 If the provision for taxation account appears only in the balance sheet. Ie opening provision net of advance tax of Rs. In either case they represent Inventory specifically held for. Interest paid 310000 Income taxes paid 1700000 Net cash from operating activities. The amount of taxes your company paid for the accounting period goes on the cash flow statement. Meanwhile some companies pay taxes before they are due such as an estimated tax payment based on what might. Under the accrual-basis accounting rules used by most companies advance payments cant be counted as revenue because the company hasnt.

OVERALL AS SAID BY PAWAN OPERATING PROFIT WILL BE DECREASED BY RS. If no payments were made the ending balance would be CU 41000. Many companies present both the interest received and interest paid as operating cash flows. However as the ending balance is only CU 16000 we can conclude that the amount of income tax paid must have been CU 25000. Advance tax tds as income tax paid and if you are preparing cash flow as per indirect method then you need to compare last years tax liability or asset as against last years tax liability or asset and show difference in income tax payment provided in balance sheet you are grouping tax paid against. Income tax paid in advance cash flow. Income Tax paid Op. It binds the Comptroller of Income Tax to apply the relevant provisions of the Income Tax Act in the manner that was set out in the ruling. Provision for Tax in Cash Flow Statement 1 If the provision for taxation account appears only in the balance sheet. Proceeds from issuance of common stock.

Meanwhile some companies pay taxes before they are due such as an estimated tax payment based on what might. Under the accrual-basis accounting rules used by most companies advance payments cant be counted as revenue because the company hasnt. Ie opening provision net of advance tax of Rs. If you paid 30000 during the last quarter and accrued a total 42000 tax. Interest paid in advance may arise as a company makes a payment ahead of the due date. Cash flows from investing activities. The tax paid in the year can be calculated by taking the opening balance of tax payable in the statement of financial position adding the tax charged in the income statement and deducting the closing balance of tax payable. Others treat interest received as investing cash flow and interest paid as a financing cash flow. Hence this tax that we paid in advance is referred to as deferred tax asset and will be adjusted in later years by debiting the deferred tax income and crediting the current tax year expense. The method used is the choice of the finance director.

The method used is the choice of the finance director. An advance ruling will only apply to the applicant and the particular arrangement that was the subject of the ruling request and where applicable to the years or periods and provisions of the Income Tax Act stated in the ruling. If you paid 30000 during the last quarter and accrued a total 42000 tax. OVERALL AS SAID BY PAWAN OPERATING PROFIT WILL BE DECREASED BY RS. Since tax for the year is paid as per the taxable profit we would be paying a greater amount of tax than is accrued according to the accounting policies. IAS 12 implements a so-called comprehensive balance sheet method of accounting for income taxes which recognises both the current tax consequences of transactions and events and the future tax consequences of the future recovery or settlement of the carrying amount of an entitys assets and liabilities. The amount of taxes your company paid for the accounting period goes on the cash flow statement. Cash flows from investing activities. If you are preparing cash flow as per direct method then you need to show actual payment ie. The net position is shown in case of operating cash flows.

Provision CY provision made - Cl. However as the ending balance is only CU 16000 we can conclude that the amount of income tax paid must have been CU 25000. It binds the Comptroller of Income Tax to apply the relevant provisions of the Income Tax Act in the manner that was set out in the ruling. The method used is the choice of the finance director. Income tax paid in advance cash flow. Others treat interest received as investing cash flow and interest paid as a financing cash flow. If you are preparing cash flow as per direct method then you need to show actual payment ie. Advance tax tds as income tax paid and if you are preparing cash flow as per indirect method then you need to compare last years tax liability or asset as against last years tax liability or asset and show difference in income tax payment provided in balance sheet you are grouping tax paid against. L Cash payments of income taxes unless they can be specifically identified with financing and investing activities. Differences between the carrying amount and tax base of assets and liabilities and.