Spectacular Post The Closing Entries To Income Summary Comparative Trial Balance In Quickbooks

Closing Entries Types Example My Accounting Course

The Income Summary account would have a credit balance of 1060 9850 credit. After preparing the closing entries above Service Revenue will now be zero. If income summary account has credit balance means it is profit and if income summary account reflects debit balance suggested lose by business operation. 2 Post the closing entries to income summary and retained earnings. The income summary balance agrees to the net income reported on the income statement. The net income or net loss for the period. There are three general closing entries that must be made. When entries 1 and 2 are posted to the general ledger the balances in all revenue and expense accounts are transferred to the Income Summary accountAfter the closing entry is posted the Dividends account is left with a zero balance and retained earnings is left with a. Income summary is a temporary account in which all the closing entries of revenue and expenses accounts are netted at the end of the accounting period and the resulting balance is considered as profit or loss. Income summary entries are a tool for closing out accounts at the end of a month quarter or year.

CLOSING ENTRIES Ask If you started a business today and you.

The closing entries are the journal entry form of the Statement of Retained Earnings. All temporary accounts must be reset to zero at the end of the accounting period. There are three general closing entries that must be made. After preparing the closing entries above Service Revenue will now be zero. Close Revenue Accounts To close the account we need to debit the revenue account and. When entries 1 and 2 are posted to the general ledger the balances in all revenue and expense accounts are transferred to the Income Summary accountAfter the closing entry is posted the Dividends account is left with a zero balance and retained earnings is left with a.

The income summary balance agrees to the net income reported on the income statement. In other words the income and expense accounts are restarted. The net income or net loss for the period. In the first and second closing entries the balances of Service Revenue and the various expense accounts were actually transferred to Income Summary which is a temporary account. Prepare a post-closing trial balance at April 30. For Income Summary calculate and enter the balance Bal before posting the entry to close out the account. Close Revenue Accounts To close the account we need to debit the revenue account and. The net result of income less. Journalize the closing entries at April 30. You take your net income from various sources and transfer them to the income summary account.

The closing entries are the journal entry form of the Statement of Retained Earnings. In other words the income and expense accounts are restarted. Income Summary Closing 47000 Step 1. Notice that a zero balance results for each revenue and expense account after the closing entries are posted and there is a 1932 credit balance in the income summary. The income summary is a temporary account used to make closing entries. 2 Post the closing entries to income summary and retained earnings. 1 Journalize the closing entrirs at April 30. If income summary account has credit balance means it is profit and if income summary account reflects debit balance suggested lose by business operation. There are three general closing entries that must be made. Post the closing entries to Income Summary and Retained Earnings.

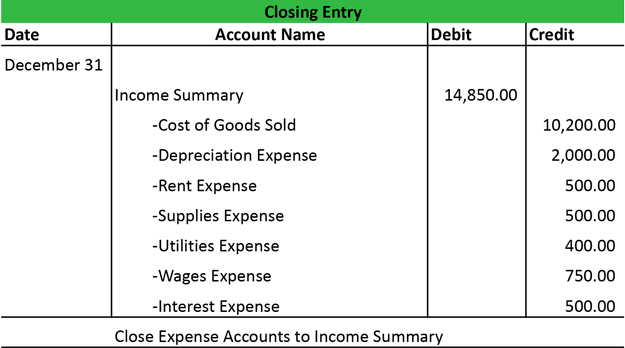

In other words the income and expense accounts are restarted. The income summary account is a temporary account used to store income statement account balances revenue and expense accounts during the closing entry step of the accounting cycle. Income summary entries are a tool for closing out accounts at the end of a month quarter or year. After posting the second closing entry to the income summary account the balance will be equal to. Closing temporary accounts to the companys income summary account allows the company to begin the next accounting cycle with a zero balance in the revenue and expense accounts. When entries 1 and 2 are posted to the general ledger the balances in all revenue and expense accounts are transferred to the Income Summary accountAfter the closing entry is posted the Dividends account is left with a zero balance and retained earnings is left with a. The net income or net loss for the period. In partnerships a compound entry transfers each partners share of net income or loss to their own capital account. To do this their balances are emptied into the income summary account. Below are some of the examples of closing entries that can be used to transfer revenue and expense account balances into income summary and from there to the retained earnings.

Post the entry to close Income Summary account on the same line as you entered the balance prior to closing the second line and then show the post-closing balance Bal on the last third line of the account. After preparing the closing entries above Service Revenue will now be zero. The goal is to make the posted balance of the retained earnings account match what we reported on the statement of retained earnings and start the next period with a zero balance for all temporary accounts. Prepare a post-closing trial balance at April 30. Closing temporary accounts to the companys income summary account allows the company to begin the next accounting cycle with a zero balance in the revenue and expense accounts. The income summary account is a temporary account used to store income statement account balances revenue and expense accounts during the closing entry step of the accounting cycle. 1 Journalize the closing entrirs at April 30. Post the closing entries to Income Summary and Retained Earnings. After closing revenue and expenses with Income summary account next step is to close income summary account because it is also nominal account and must close at the end of each account period. Income summary entries are a tool for closing out accounts at the end of a month quarter or year.

In other words the income summary account is simply a placeholder for account balances at the end of the accounting period while closing entries are being made. Journalize the closing entries at April 30. Close Revenue-Transfer close the balances of the Step 2-Transfer close the balances of the expense accounts to the Income. To do this their balances are emptied into the income summary account. Below are some of the examples of closing entries that can be used to transfer revenue and expense account balances into income summary and from there to the retained earnings. Income Summary Closing 47000 Step 1. In the first and second closing entries the balances of Service Revenue and the various expense accounts were actually transferred to Income Summary which is a temporary account. After posting the second closing entry to the income summary account the balance will be equal to. The income summary account is a temporary account used to store income statement account balances revenue and expense accounts during the closing entry step of the accounting cycle. The closing entries are the journal entry form of the Statement of Retained Earnings.