Fine Beautiful These 16 Accounts Are From The Adjusted Trial Balance Statement Of Owners Equity Accounting

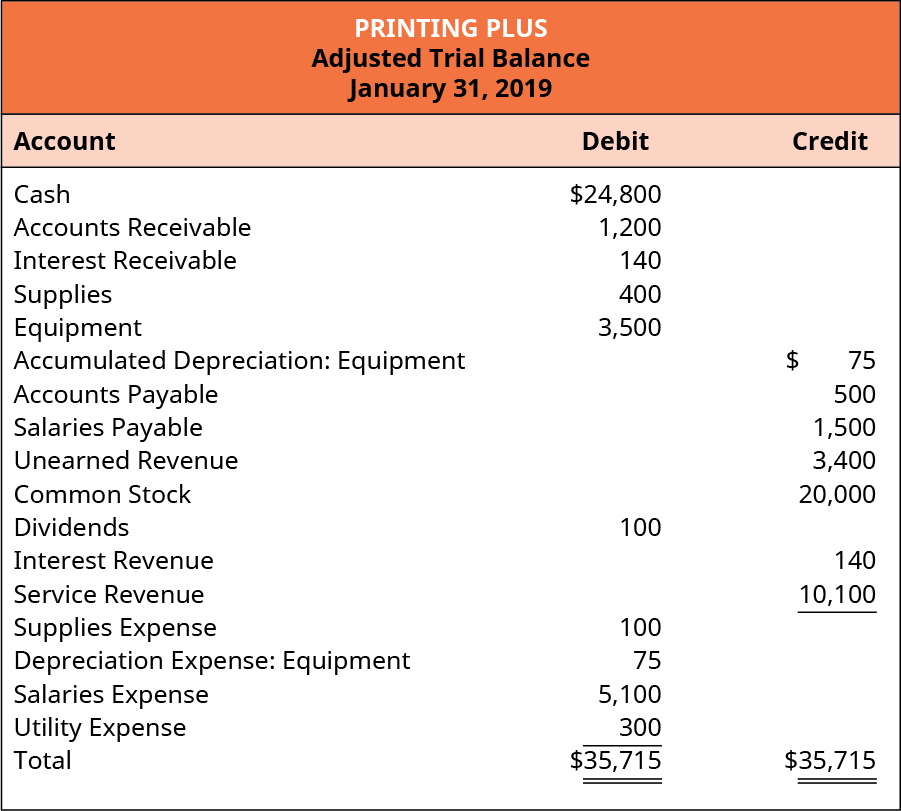

Use The Ledger Balances To Prepare An Adjusted Trial Balance Principles Of Accounting Volume 1 Financial Accounting

The adjusted version of a trial balance may combine the debit and credit columns into a single combined column and add columns to show adjusting entries and a revised ending balance as is. BALANCE SHEET DEBIT CREDIT DEBIT CREDIT DEBIT Cash Accounts Receivable Supplies Prepaid Rent. These 16 accounts are from the Adjusted Trial Balance columns of a companys 10-column work sheet. In the blank space beside each account write the letter of the appropriate financial statement column A B C or D to which a normal account balance is extended. Thus it should always be prepared after the trial balance. Credit column for the Income Statement columns. Debit column for the income statement. Debit column for the Income Statement columns. An adjusted trial balance is prepared from the general ledger. The accounts that do not have adjustments are extended from the Trial Balance section to the Adjusted Trial Balance section.

The trial balance is a list of all the accounts a company uses with the balances in debit and credit columns.

An adjusted trial balance is prepared from the general ledger. These 16 accounts are from the Adjusted Trial Balance columns of a companys 10-columun work sheet. Adjusting entries are prepared at the end of the accounting period for. Debit column for the Income Statement columns. ADebit column for the Income Statement columns. These 16 accounts are from the Adjusted Trial Balance columns of a companys 10-column work sheet.

BALANCE SHEET DEBIT CREDIT DEBIT CREDIT DEBIT Cash Accounts Receivable Supplies Prepaid Rent. Select the letter of the financial statement column A B C or D where a normal account balance is extended. Debit column for the Income Statement columns. Debit column for the income statement. Debit column for the Income Statement columns. The intent of adding these entries is to correct errors in the initial version of the trial balance and to bring the entitys financial statements into compliance with an accounting framework such as Generally Accepted Accounting Principles or International Financial Reporting. All accounts having an ending balance are listed in the trial balance. In the blank space beside each account write the letter of the appropriate financial statement column A B C or D to which a normal account balance is extended. An adjusted trial balance is prepared after adjusting entries are made and posted to the ledger. These accounts are from the Adjusted Trial Balance columns in a companys 10-column work sheet.

These 16 accounts are from the Adjusted Trial Balance columns of a companys 10-column work sheet. We can post these transactions using T-accounts or ledger cards. Thus it should always be prepared after the trial balance. These 16 accounts are from the Adjusted Trial Balance columns of a companys 10-columun work sheet. An unadjusted trial balance is prepared from the general ledger. Debit column for the Income Statement columns. Adjusting entries are prepared at the end of the accounting period for. There are three types of trial balances. The adjusted version of a trial balance may combine the debit and credit columns into a single combined column and add columns to show adjusting entries and a revised ending balance as is. The accounts reflected on a trial balance are related to all major accounting Accounting Accounting is a term that describes the process of consolidating financial information to make it clear and understandable for all items including assets Types of Assets Common types of assets include current non-current physical intangible operating and non-operating.

Adjusted trial balance includes the following accounting entries which are not included in the trial balance. An unadjusted trial balance is prepared from the general ledger. These 16 accounts are from the Adjusted Trial Balance columns of a companys 10-column work sheet. Adjusting entries are journalized. In the blank space beside each account write the letter of the appropriate financial statement column A B C or D to which a normal account balance is extended. Debit column for the Income Statement columns. These 16 accounts are from the Adjusted Trial Balance columns of a companys 10-columun work sheet. The accounts that do not have adjustments are extended from the Trial Balance section to the Adjusted Trial Balance section. In the blank space beside each account write the letter of the appropriate financial statement column A B C or D to which a normal account balance is extended. Debit column for the Income Statement columns.

Debit column for the Income Statement columns. An unadjusted trial balance is prepared from the general ledger. In the blank space beside each account write the letter of the appropriate financial statement column A B C or D to which a normal account balance is extended. Credit column for the income statement. Adjusting entries are prepared at the end of the accounting period for. There are three types of trial balances. Adjusting entries are journalized. ADebit column for the Income Statement columns. We are using the same posting accounts as we did for the unadjusted trial balance just adding on. These 16 accounts are from the Adjusted Trial Balance columns of a companys 10-column work sheet.

Adjusted trial balance includes the following accounting entries which are not included in the trial balance. Credit column for the income statement. All accounts having an ending balance are listed in the trial balance. Debit column for the Income Statement columns. C 367 a 1000 b 3500 c 367 a 1000 b 3500 83500 5000 22000 7000 90000 4000 7000 500 35000 CREDIT ADJ. The intent of adding these entries is to correct errors in the initial version of the trial balance and to bring the entitys financial statements into compliance with an accounting framework such as Generally Accepted Accounting Principles or International Financial Reporting. Select the letter of the appropriate financial statement column A B C or D to which a normal account balance is extended. Debit column for the Income Statement columns. The accounts reflected on a trial balance are related to all major accounting Accounting Accounting is a term that describes the process of consolidating financial information to make it clear and understandable for all items including assets Types of Assets Common types of assets include current non-current physical intangible operating and non-operating. These 16 accounts are from the Adjusted Trial Balance columns of a companys 10-column work sheet.