Casual Us Gaap Cash Flow Statement Example Self Employed Monthly Income

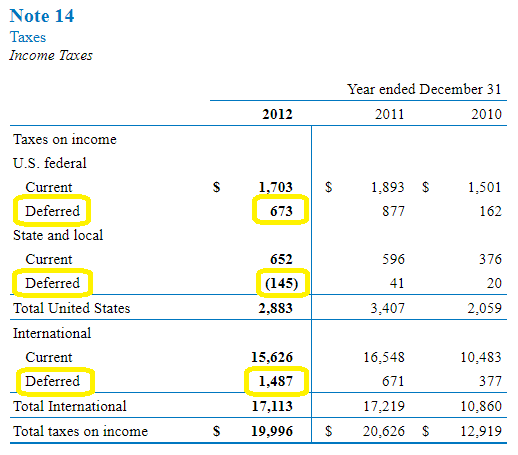

Deferred Income Tax Liabilities Explained With Real Life Example In A 10 K

Add paragraphs 230-10-50-7 through 50-8 and their related heading with a. Moreover expenses and related liabilities generally are recorded before the disbursement of cash. It reflects certain captions required by ASC 230 bolded and other common captions. Statement of Cash Flows Example. For the Year Ended December 31 2011. Composed of actions related to the sale of products or services it records expenses for raw materials acquisition marketing expenses sale expenses tax payments and more 2. Thus the statement of cash flows is actually enhanced to reveal the totality of investing and financing activities whether or not cash is actually involved. Statement of cash flows shall report that information in a manner that reconciles beginning and ending totals of cash cash and cash equivalents and amounts generally described as restricted cash or restricted cash equivalents. Cash Flow from Financing Activities. CASH FLOWS FROM OPERATING ACTIVITIES Cash received from contributions 5986000 3741000 Cash payments to employees and vendors 5128000 4620000 Cash payments from related parties net 393000 303000 Interest and dividends received 29000 13000.

An Example of Detailed Statement of Cash Flows.

Its an asset not cashso with 5000 on the cash flow statement we deduct 5000 from cash on hand. Decrease in non-cash current assets -- add-- Example. Collection of accounts receivable. Cash Flow from Investing Activities in our example Purchase of Equipment is recorded as a new 5000 asset on our income statement. Composed of actions related to the sale of products or services it records expenses for raw materials acquisition marketing expenses sale expenses tax payments and more 2. GAAP requires that assets and liabilities as well as revenues and expenditures be recorded on the accrual basis of accounting.

Add non-cash expenses--- Example. Learn how to analyze Amazons consolidated statement of cash flows in CFIs Amazon Advanced Financial Modeling Course. These cash flows are generally associated with the purchase or sale of assets. Moreover expenses and related liabilities generally are recorded before the disbursement of cash. Cash Flow from Financing Activities. Below is an example from Amazons 2017 annual report which breaks down the cash flow generated from operations investing and financing activities. Thus the statement of cash flows is actually enhanced to reveal the totality of investing and financing activities whether or not cash is actually involved. This means that assets are often reported and revenues are recognized before the receipt of cash. The net Cash Flow Statement of the company remains the same. From dawn till dusk for days on end I wrestled with that wheel.

Learn how to analyze Amazons consolidated statement of cash flows in CFIs Amazon Advanced Financial Modeling Course. Decrease in non-cash current assets -- add-- Example. For the Year Ended December 31 2011. Cash Flow from Investing Activities in our example Purchase of Equipment is recorded as a new 5000 asset on our income statement. Example cash gaap statement flows us of William Faulkner was born into a wealthy family in William Faulkner was born into a wealthy family in and lived almost his entire life in Mississippi. Statement of Cash Flows. As I said before both the cash inflows and outflows are considered. Cash Flow from Financing Activities. Depreciation and amortization 2. Cash Flows from Operating Activities.

Statement of cash flows shall report that information in a manner that reconciles beginning and ending totals of cash cash and cash equivalents and amounts generally described as restricted cash or restricted cash equivalents. GAAP the statement of cash flows includes a separate section reporting these noncash items. Not all captions are applicable to all reporting entities. This means that assets are often reported and revenues are recognized before the receipt of cash. Collection of accounts receivable. Cash Flows from Operating Activities. Composed of actions related to the sale of products or services it records expenses for raw materials acquisition marketing expenses sale expenses tax payments and more 2. The cash flow from operating activities. It reflects certain captions required by ASC 230 bolded and other common captions. GAAP requires that assets and liabilities as well as revenues and expenditures be recorded on the accrual basis of accounting.

The cash flow from financing activities is composed of debentures shares notes payments of dividends. An Example of Detailed Statement of Cash Flows. IFRS vs GAAP can bring a major change in the Cash Flow of Activities. Not all captions are applicable to all reporting entities. Statement of Cash Flows Example. GAAP requires that assets and liabilities as well as revenues and expenditures be recorded on the accrual basis of accounting. Its an asset not cashso with 5000 on the cash flow statement we deduct 5000 from cash on hand. The cash flow statement CFS measures how well a company manages its cash position meaning how well the company generates cash to pay its debt obligations and fund its operating expenses. Subtract gain on sale of property plant and equipment-- Gain on sale of property plant and equipment is included-- in cash flows form investing activities 3. These cash flows are generally associated with the purchase or sale of assets.

Add non-cash expenses--- Example. For the Year Ended December 31 2011. Statement of cash flows Prepared by. Cash Flow from Investing Activities in our example Purchase of Equipment is recorded as a new 5000 asset on our income statement. Depreciation and amortization 2. An Example of Detailed Statement of Cash Flows. Not all captions are applicable to all reporting entities. Add paragraphs 230-10-50-7 through 50-8 and their related heading with a. The cash flow from financing activities is composed of debentures shares notes payments of dividends. Statement of cash flows shall report that information in a manner that reconciles beginning and ending totals of cash cash and cash equivalents and amounts generally described as restricted cash or restricted cash equivalents.